The interest rate cutting cycle has begun; Time to invest internationally as the US dollar weakens against major currencies.

Lower US inflation and falling interest rates will pressure the US dollar going forward, making US assets less attractive.

The Fed announced a 50 basis point cut on 18 September.

In the accompany statement at the meeting, the Federal Reserve said that “the upside risks to inflation have diminished and the downside risks to employment have increased.” It is clear, that the Fed is now more concerned about growth conditions in the US economy, rather than inflation.

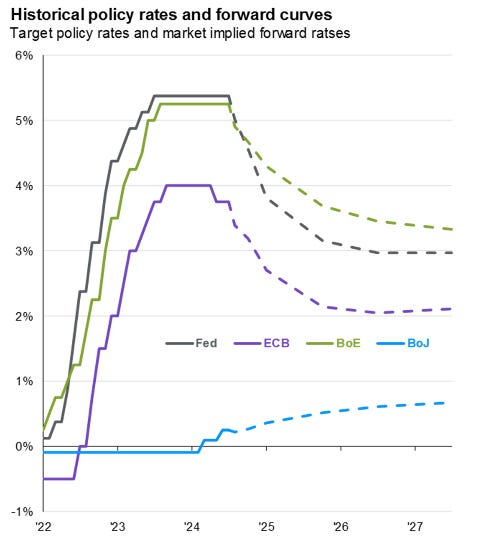

With the start of the rate cutting cycle, the Federal Reserve, together with other major central banks is expected to continue lowering interest rates up till 2026.

The Bank of Japan, however, is an exception to other economies as they are projected to raise interest rates over time.

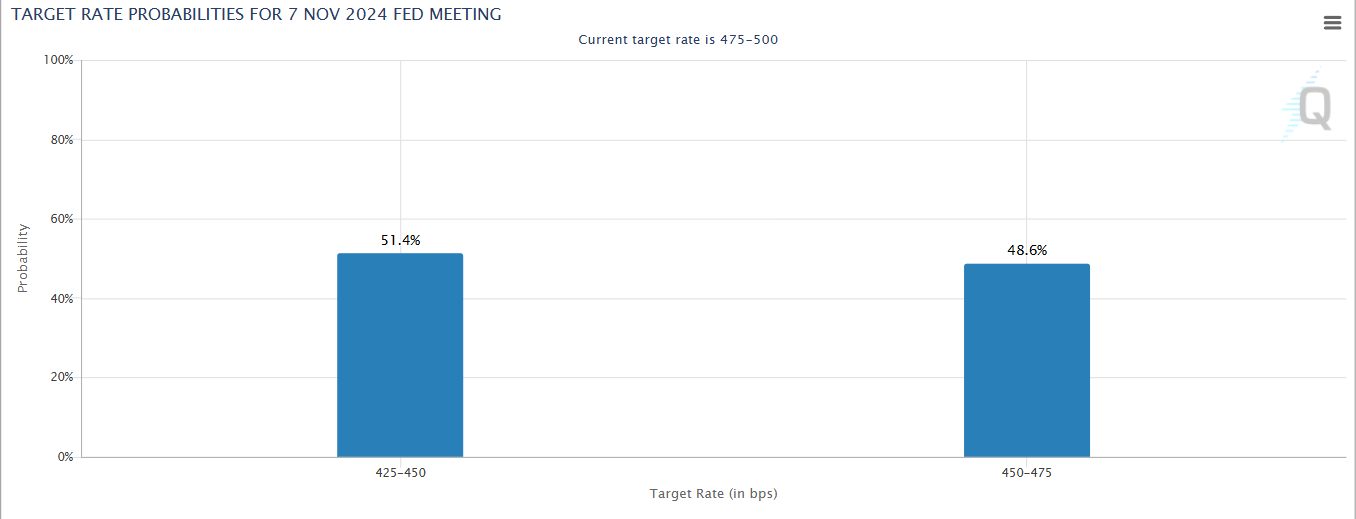

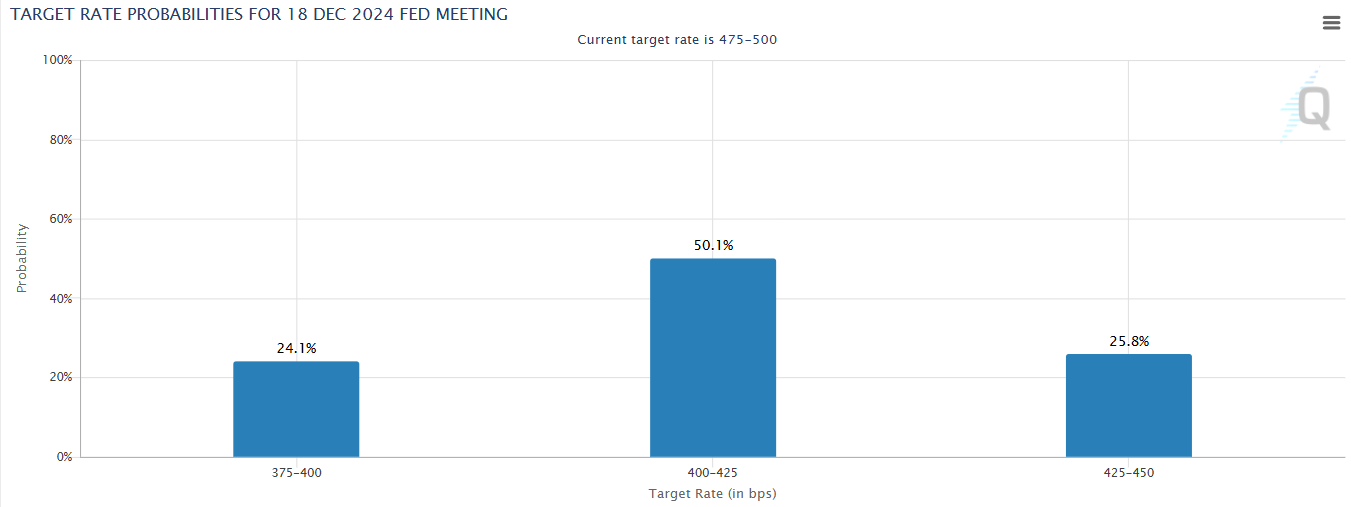

Implied Interest rate Probabilities

As of 20 September, the Fed funds futures market is uncertain whether the Fed will cut interest rates at the 7 November meeting.

Yet, most participants expect further rate cuts in December.

This suggest that the Fed funds futures market is hawkish about a November outcome (i.e., a pause in interest rate cuts) possibly because participants are focused on the rosy estimates for US real GDP in the updated Summary of Economic Projections, which upgraded US real GDP growth of 2% every year through 2027.

US long term economic forecast

But in reality, an annual GDP growth rate of 2% is considerably weak in my opinion, as estimates from the US Congressional Budget Office point to 2.9% growth in 2024, but a step down to 2% in 2025 and in 2026.

Further, the table above also shows that unemployment weakness is likely to persist up till 2027 (rising to 4.5% in the long run), although the good news is that headline inflation will fall towards the Fed’s 2% target by the end of 2025.

Nonfarm payrolls, as seen in the chart on the left, indicate weakening job growth. Additionally, labour force expansion has been driven pretty much by US foreign immigration.

Lower interest rates and implications on equity market returns

As US interest rates decline, US Treasury yields are expected to follow suit and head lower. With lower bond yields, historically, US equity market returns actually fall when the 10-year yield decreases to a range of 3-4%

As a matter of fact, international equities have outperformed US equities when Treasury yields decline to a 2-3% range.

This makes the investment case for international stocks

As the Fed embarks on its interest rate cutting cycle, the dollar is projected to weaken (at least for around 40 weeks according to PIMCO), suggesting that international assets are comparatively more attractive than the US.

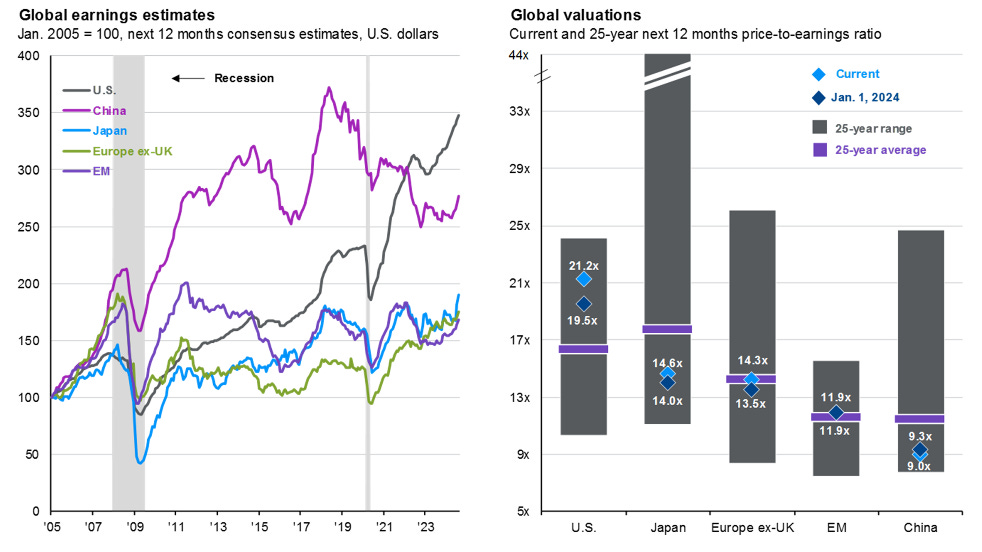

Among them, Japanese stocks do look appealing as earnings estimates have continued to exceed new highs (see the chart on the left). Investors may also consider Europe ex UK as earnings for Europe ex UK have also increased.

Secondly, from a valuation perspective, Japan is cheap as P/E ratios are below its 25-year average (as illustrated in the right chart).

From the PMI surveys, the global economy is still in a healthy state. Global PMIs was 52.5 in July, supported by an expanding services sectors. The manufacturing sector has been contracting, but gradually improving.

Japan PMIs have been growing, increasing from 52.5 in July to 53.0 in August. The Euro area has meanwhile emerged from a recession, rising from 50.2 to 51.2 over the same period. Other notable areas of strength are India and Brazil although the stock valuations for these countries are too frothy at the moment.

Japan has been benfetting from the weak Yen. Many Japanese companies, especially the banks have deployed assets overseas over many years. The weak currency gives a strong FX translational boost to their earnings. As well as exporters, on the back of higher demand for Japanese exports. However, near term, I do see some selling pressure on the USDJPY pair, which might limit the upside for Japanese stocks. But over the longer term, investor interest in Japan is expected to remain high.

With the above in mind, I do not feel highly convicted to add any stock to the live portfolio. Our model has not triggered any strong buy signals since the small cap ETF investment in July. Overall, I maintain the view that equities will continue rising, but the path forward will be rocky and possibly more volatile than the last nine months. If you are a trader, I think selling rallies and buying dips is a good strategy.

Disclaimer

Seven Fat Cows is not a financial adviser. You should seek independent legal, financial, or other advice to check if the information from this website relates to your unique circumstances.